Private pension provision: What the self-employed should look out for

Never forget: Time is money! Thinking about tomorrow today. Speak, retirement planning. This is important for everyone – but especially for the self-employed. This is because many of them are not members of the statutory pension insurance scheme.

This means that the self-employed have to take their old-age provision into their own hands. And even if self-employed people pay into the statutory pension fund, they should make additional private provision and start as early as possible.

Some self-employed persons are obliged to pay into the statutory pension insurance. These include craftspeople, artists, publicists, physical therapists, nurses, and freelance teachers. The Social Code VI (SGB VI, paragraph 2) regulates which occupational groups are subject to compulsory insurance

Some occupational groups of the self-employed must pay into the statutory pension fund

Those who are compulsorily insured as self-employed generally pay 18.6 percent of their income into the pension insurance scheme. It should be noted, however, that self-employed persons can expect a rather low pension benefit. For this reason, self-employed persons with compulsory insurance should also make other private provisions for old age.

Those who work as freelancers in so-called chamber professions are compulsorily insured there – and pay income-dependent compulsory contributions. These include doctors, lawyers, pharmacists and architects.

Voluntarily insured persons can co-determine the amount of their contributions

However, the majority of the self-employed must take out voluntary insurance. You can also pay into the statutory pension insurance scheme – on a voluntary basis.

This is supported by the fact that, in addition to coverage for old age, survivor protection for spouses, registered partners and orphans is always included.

Insured persons can determine the amount of voluntary contributions themselves – the minimum contribution is 83.70 euros, and the maximum contribution is around 1,320 euros per month. Insured persons may pay voluntary contributions monthly or once a year.

What applies to compulsorily insured self-employed persons?

- Within five years of starting their own business, self-employed persons can apply for compulsory pension insurance. One of the advantages: Compulsorily insured self-employed persons secure entitlements to rehabilitation or a pension due to reduced earning capacity.

- Self-employed persons can pay the compulsory contributions either as a standard contribution or according to their actual income. Currently, the standard contribution in the western states is around 612 euros per month and around 586 euros in the eastern states. It is also possible to pay half of the regular contribution in the year of starting the activity and in the three following calendar years.

- In any case, the following applies to the statutory pension insurance: There are no additional costs or a health check. The statutory pension insurance also covers parts of the health insurance, up to 50 percent of the contribution, if a pension is paid.

Alternatives and additional coverage options for old age. This much in advance: the Riester is NOT it!

- In addition to paying into the statutory pension insurance, self-employed persons have other options for private provision. For example, you can take out a so-called Rürup contract, which is available in the form of a classic or unit-linked pension insurance.How high the pension will be one day depends, among other things, on the contributions paid in and the exact terms of the contract. The amount of the contribution payment is flexible. The insured can usually adjust the contributions at any time to suit their own needs or benefits.A Rürup pension, however, usually only covers old-age provision. Insured persons can add the modules survivor protection and reduction in earning capacity if required, but this usually involves additional costs. This can have an impact on returns.But a Riester contract doesn’t cut it either, because the statutory guarantee obligation for contribution payments means that contributions can be invested almost exclusively only in government bonds. And they are profitable negatively! This almost guarantees that the Riester contract is dead in terms of returns.

6% and more with the private pension and much higher flexibility for self-employed people.

If you want to see how 6.73% return p.a. or more can be achieved through the capital market, apply for Genève Invest’s investment results, certified by the auditor (BDO), here:

Now is the ideal window of opportunity to invest in bonds. Corporate bonds currently offer yields in excess of 7% p.a.

Arrange a callback from one of our experts now. We advise you free of charge & without obligation and find the best corporate bonds for you.

For investors with €100,000 or more

Free consultation & callback service

Depending on the client’s needs, Genève Invest invests the funds entrusted to it in high-quality equities, corporate bonds and alternative investments. To ensure the highest level of transparency, we have analyzed the overall performance of our client portfolios and had the results and methodology audited by the auditing firms KPMG & BDO Switzerland (there will also be another performance audit in 2023, including the 2022 figures).

Our performance results for our investment strategies:

- In the fixed income category, assets in the portfolio were invested in corporate bonds or investment funds that invest exclusively in corporate bonds. Genève Invest has achieved an overall performance of 123.4% (6.4% p.a.).

- In the “Income plus Yield” category, a maximum of 30% of the assets in the portfolio were invested in equities, alternative investments or equity funds, and the remaining assets were invested in corporate bonds or investment funds that invest exclusively in corporate bonds. Genève Invest has achieved an overall performance of 163.4% (7.7% p.a.).

- In the “Balanced Portfolio” category, a maximum of 70% of the assets in the portfolio were invested in equities, alternative investments or equity funds, and the remaining assets were invested in corporate bonds or investment funds that invest exclusively in corporate bonds. Genève Invest has achieved an overall performance of 237.8% (9.8% p.a.).

- In the Dynamic Portfolio category, more than 70% of the assets in the portfolio were invested in equities, alternative investments or equity funds, and the remaining assets were invested in corporate bonds or mutual funds that invest exclusively in corporate bonds. Genève Invest has achieved an overall performance of 287.2% (11% p.a.).

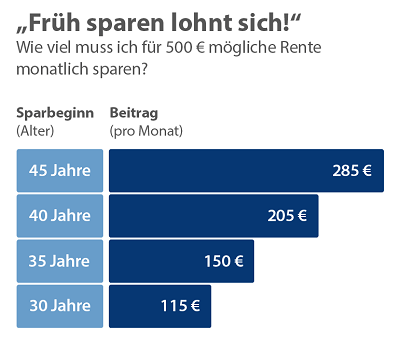

Never forget: Especially as a self-employed person, it is best to make private provisions for old age as early as possible. After all, time is money.

CONCLUSIONS:

Without question, it’s worthwhile for the self-employed to seek independent advice about their retirement savings and protection in the event of reduced earning capacity. This is possible, for example, through a competent advisor from an independent asset management company.

CTA: If you would like to arrange a personal consultation with an investment expert on the topic of “private retirement planning”, please use our free initial consultation.