In this way, savers find a solid investment with a high return

Security and high interest rates are said to be mutually exclusive. In practice, however, savers can also achieve attractive returns with a solid investment.

Achieving attractive returns with bonds or other interest-bearing investments has not been easy in recent years. This is due to the zero interest rate policy and the bond purchase programs of the central banks. Even government bonds from countries like Greece or Italy have recently offered little more yield than German government bonds. Finding reasonably safe interest rate investments that also offer a significant return seems like the proverbial search for a needle in a haystack. But this search is by no means hopeless. The market offers savers who know how to assess the opportunities and risks correctly enough good opportunities for successful investments in bonds. It is important to properly understand the interaction between risk and return.

These factors essentially determine the return potential of bonds:

- Nominal interest rate of the bond

- market rate

- creditworthiness of the debtor

- term of the bond

According to conventional wisdom, safety and return are two ends of the same scale

Basically, when investing, the higher the chance of a high return, the less security it offers. If savers invest in an investment that promises disproportionately high interest rates, these investors also run a higher risk that interest payments will not be made or that repayment will not be made. The equation also applies in reverse. The more security an investment offers, the lower the expected return.

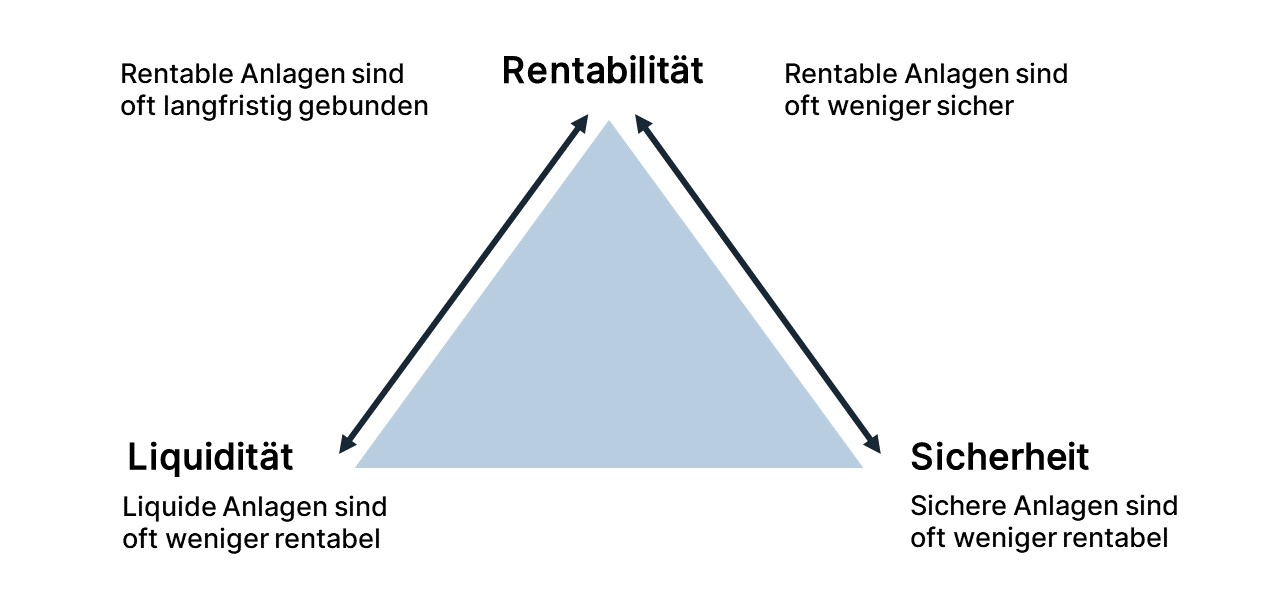

Yield, security and liquidity are interrelated. You can find out more about the “magic investment triangle” here .

The eternal interplay of risk and return

It is not for nothing that interest rates contain a risk premium. This is because the amount of return on an investment is made up of several factors. The basis is the so-called risk-free interest rate. This means an investment in which savers can be almost certain that they do not run the risk of losing their invested capital when making an investment. The yields on federal bonds are often used as a reference value. Another factor is the remaining term of an interest-bearing investment, such as a bond. As a rule, the longer the remaining term of an interest-bearing investment, the higher the return. Here, too, risk is priced in. Because the further events are in the future, the greater the uncertainty about the further course. Who can see into the future? And the same applies to other risk factors when it comes to the term: more uncertainty equals more risk equals higher returns.

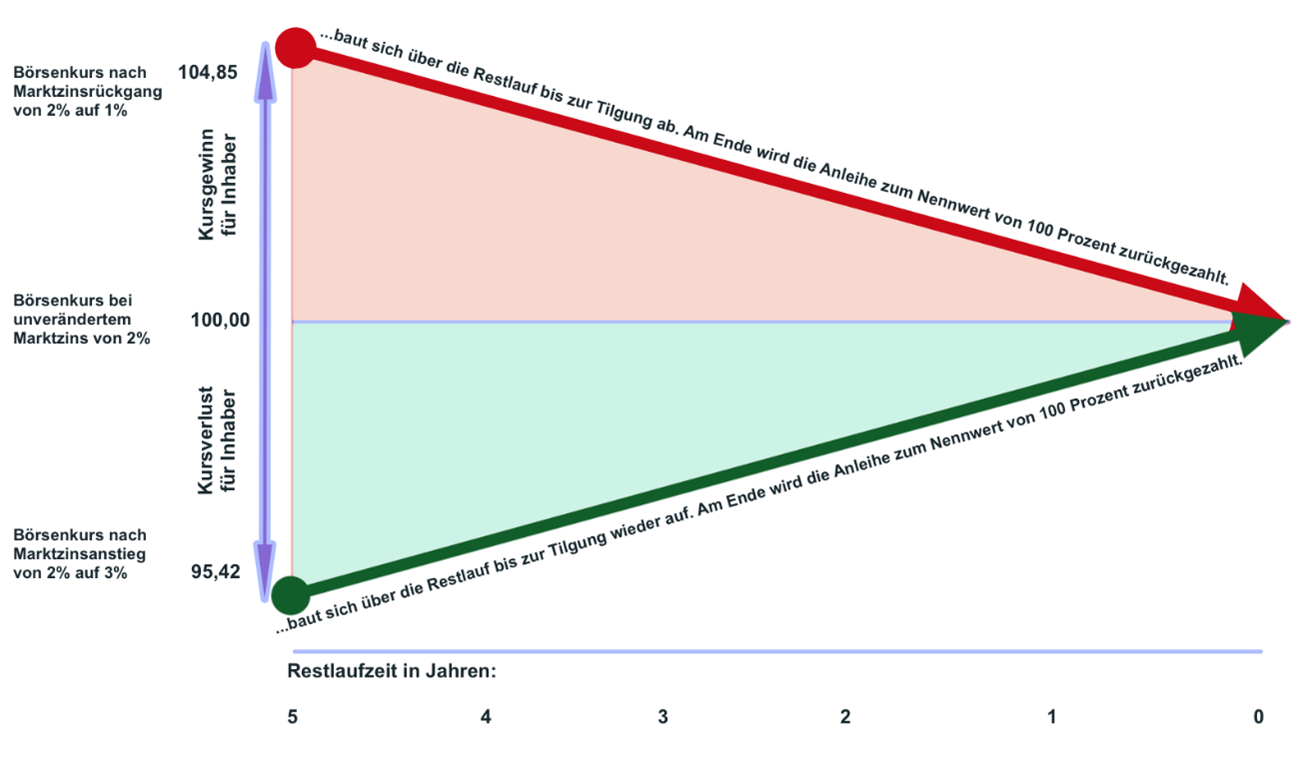

Effects of a change in the market interest rate on the market price of a federal bond with a remaining term of 5 years and a coupon of 2%.

Scenario 1: If the market interest rate remains unchanged compared to when the bond was issued, the market price of the bond does not change either. Scenario 2 : If the market interest rate rises from 2% to 3%, the bond price falls. Bondholders would have to accept price losses if they were to be sold. Investors who buy the bond for the first time achieve a higher return in the amount of the new market interest rate of 3%, since they can buy in at a lower price and record price gains until the end of the term. Scenario 3: If the market interest rate falls from 2% to 1%, the price rises. Bondholders could make a price gain by selling immediately. Investors who buy the bond again have to pay this higher price when they buy it and have to accept a price loss until the end of the term, since the price of the bond gradually falls to 100 percent of the nominal value until the end of the term. The yield that can be achieved on the bond until the end of the term corresponds to the new market interest rate of 1%.

How creditworthiness affects the price of a bond

Another factor is the creditworthiness of the respective debtor. Federal bonds are considered risk-free because investors can be almost certain that the Federal Republic will pay their interest and settle their debts. This is not the case with other borrowers such as certain emerging markets or companies. Depending on the market assessment of their respective creditworthiness, they have to offer savers an interest premium – i.e. a risk premium. And so it happens that bonds from a company that has done poorly in recent years and where investors fear that there may be a risk of bankruptcy are, experience has shown, to be much cheaper and therefore offer a better return than bonds from a large corporation that is considered the market leader and whose business will be good for the foreseeable future.

How does your portfolio perform?

We show you how Genève Invest can improve your portfolio.

Get personalized advice on diversification, cost minimization and efficiency.

Great opportunities through market inefficiencies

The assessment of market participants as to how secure the repayment and expected interest payments of an investment are is a decisive factor for the amount of the expected return. At the same time, the key to success for alert investors lies in the word “assessment”. Because the “market” can misjudge. This is not uncommon, especially with corporate bonds. There are mutliple reasons for this. One reason is that some large market participants such as insurance companies or pension funds are being forced to buy safer government bonds. They can therefore only act freely within a certain framework and are not buyers of many corporate bonds. For this reason alone, government bonds are more expensive on average and offer less yield than corporate bonds. Another reason is, Rating agencies such as Moody's or Fitch do not rate all bonds. And even the analysts of large institutional investors only ever have their eye on a sub-segment of the huge bond market. Companies outside the big observed mainstream therefore have to offer higher interest rates in order to find investors for their bonds. But that doesn't mean these companies are less likely to pay their interest and return the money they borrowed through bonds to investors. There is only more uncertainty about this due to a lack of analysis. The formula applies here: Less knowledge equals more uncertainty equals more returns.

The credit rating does not say everything about the safety of a bond

Another opportunity lies in the fact that “the market” often evaluates the wrong criteria. When a company's business isn't performing as "the market" expects, it usually means the company's stock price falls. Because the profit forecasts have to be adjusted downwards if business development is disappointing. This reduces the value of the company - and with it its valuation on the stock exchange. However, different rules apply to the valuation of bonds than to stocks. All that matters with bonds is whether a company can make its interest payments and repay its debt. Whether a company makes higher or lower profits is only of interest to bondholders if there is a risk of insolvency. Nevertheless, bond prices often fluctuate in connection with published business figures or rumours. Investors who act coolly on the interest rate market often have good investment opportunities.

WHY CORPORATE BONDS NEED TO BE IN EVERY PORTFOLIO

Geneve Invest is an asset management company with more than 20 years of experience and over 1,000 clients. Thanks to these decades of experience, we are able to give you, as a private investor, valuable first-hand insights into the area of profitable asset management.

Which return chance which investment offers

Another factor is the creditworthiness of the respective debtor. Federal bonds are considered risk-free because investors can be almost certain that the Federal Republic will pay their interest and settle their debts. This is not the case with other borrowers such as certain emerging markets or companies. Depending on the market assessment of their respective creditworthiness, they have to offer savers an interest premium – i.e. a risk premium. And so it happens that bonds from a company that has done poorly in recent years and where investors fear that there may be a risk of bankruptcy are, experience has shown, to be much cheaper and therefore offer a better return than bonds from a large corporation that is considered the market leader and whose business will be good for the foreseeable future.

How creditworthiness affects the price of a bond

There is a lot of talk about bonds in the above examples. That's because almost every interest rate investment is based on bonds. Money deposited by investors in savings accounts at a bank or invested as a time deposit is mainly invested by the banks in bonds, but also in other asset classes that promise higher returns. The difference between the interest that the bank pays investors and the return that the bank generates on the capital market with the deposited investor money flows to the bank as profit. It is therefore not uninteresting for savers to know which asset classes exist and how much return they can offer.

The following investment classes exist:

- Bank deposits such as cash, savings accounts and time deposits

- property

- raw materials

- Fixed income securities such as government bonds, mortgage bonds and corporate bonds

- Shares

- Bank deposits such as cash, savings accounts, and time deposits: 0–3%

- Real estate: 3–5%

- Raw Materials: 1-3%

- Fixed income securities such as government bonds, mortgage bonds and corporate bonds: 0-7%

- Stocks 7-10%

Now is the ideal time to invest in bonds. Corporate bonds currently offer yields of over 7% pa

Arrange a callback from one of our experts now. We advise you free of charge and without obligation and find the best corporate bonds for you.

For investors with €100,000 or more

Free advice & callback service

Equities and bonds combined: The Genève Invest concept

The highest returns can be achieved with equity investments or dynamic investment strategies achieve. In the short term, larger price fluctuations are possible here than with other asset classes. In the long run, the experience looks different. For example, the longest period of losses in the DAX in the past 30 years stretched over seven years, from 2001 to 2007. Investors who had invested in the DAX immediately before the dot.com bubble burst in March 2000 would be after 6 years been back in the black. Mind you: This is only the worst-case scenario. At the same time, it means that in the past 30 years all other entry points than just before the crash in 2000 have led to significantly shorter loss phases or directly to profits. That's about 7-10% gains per year, depending on the calculation method. Investors can manage their investment risk relatively well with a combination of stocks and bonds. Bonds with a high credit rating can then be used as a stabilizer, while stocks deliver the returns. If you follow the principle of value investing - i.e. the search for undervalued stocks and bonds - with both asset classes, sustainable solid returns can be achieved. The mixed fund Global Income – Interest & Dividend (ISIN: LU0388926494) has proven this regularly in recent years. The bottom line is that the mixed fund has achieved an average increase in value of more than ten percent per annum since it was launched in 2012.

The fact is: stocks offer the highest returns!

Rented properties offer a steady flow of capital

Comparatively high returns can also be achieved with rented properties . Different rules apply here than for stocks or bonds. Perhaps the most important difference: Real estate, as the name suggests, cannot be bought or sold quickly. The invested money is tied up and not liquid. Another important difference to stocks or bonds is that the current value of a property can only be estimated. Buyers and sellers only find out how much a property is worth on the day the contract is signed.

Gold is considered insurance against major crises

When we talk about commodities as an investment, we specifically mean gold . Because all other types of investments in commodities are usually either hedging transactions or speculation. Such investments are not worthwhile for private investors. And gold is not a long-term investment either, but a kind of insurance against crises. Because gold pays no interest and no dividends. On the contrary. Storing gold costs money.

The Geneve Invest concept

Corporate bonds with high yield and best risk/return ratio

Systematic focus on niche topics and special factors

Continuous and predictable revenue flow

Legal protection for bondholders: focus on secured senior bonds

Forward-looking & transparent communication with company management

Lower fluctuations in value than shares and advantages of effective diversification

Fixed high bond rates & reduction of yield curve risk.

Additional earnings by exploiting the yield curve effect